Uncertainty on the Horizon

Economic Update

For December, the U.S. manufacturing rate was 49.3% on the ISM Index, 0.9% higher than the November reading. Any reading under 50.0% is contractionary, marking the 25th time in the last 26th months that manufacturing activity contracted. The unemployment rate decreased to 4.1% in December, adding 256,000 jobs. The report presents a picture that the labor market has slowed but is still doing well. The job gains were primarily in healthcare, social assistance, government, and leisure and hospitality. The central bank now faces a dilemma with a strong job market and sticky inflation, likely slowing the pace of rate cuts this year.

State of Corporate Credit

S&P Global Ratings has recently downgraded several issuers to Default (D) or Selective Default (SD) in recognition of distressed exchanges, only to upgrade them shortly after. However, the subsequent upgrades were primarily to ‘CCC(+X-)’ ratings, which is well into the junk rating territory. This shows that even though companies can extend their debt maturities through distressed exchanges, their overall financial position, and credit risk, remain very poor. These transactions are tantamount to a default and are essentially prolonging the debt maturities but not addressing the unsustainable debt load and high interest payments.

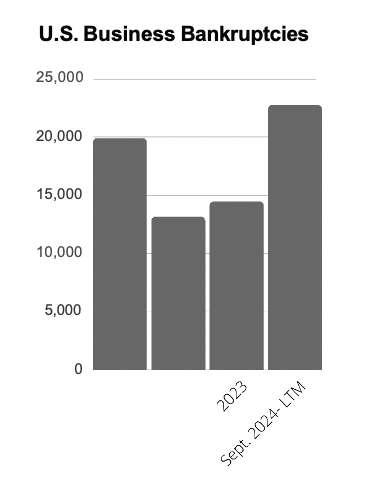

Insolvencies

U.S. Corporate bankruptcy filings soared in December 2024 to a 14 year high. The 2024 total surpassed the 2020 filings total, a prevous 1G-year high set during a year that was significantfy impacted by the COVID-19 pandemic. The 2024 total is the largest single year-talfysince 2010, during the aftermath of the Great Recession. In Canada, business

insolvencies for the 12-month period ending November 31, 2024, increased by 13.4% compared with the same period last year.

Current & Evolving Credit Risks

Commodity Market Pricing

In the U.S., rising commodity prices are being driven by tariff and trade policy uncertainties, while globally, metal markets are declining due to a stronger dollar and weaker demand forecasts from China and Europe. Heading into 2025, businesses will face continued pressures on pricing both domestically and internationally. Overall, global tariffs have a bearish effect on overall commodities demand.

Heavy Truck Outlook

The heavy truck industry continues to experience a cyclical downturn, with sales projected to remain largely flat in 2025, though there may be slight increases. This outlook will likely negatively impact credit quality for marginally rated casting companies and other suppliers.

Second “China Shock”

Chinese factories are being run with a goal of maximizing employment and gaining market share over short-term profits. In almost every industry, rising Chinese exports poses a significant challenge. Within the U.S., there are existing protectionist policies, such as tariffs, that are likely to increase. However, the biggest challenge is in export markets, such as Latin America, as governments would gladly allow cheaper imports without a domestic industry to protect.