U.S. Corporate Bankruptcies Near 14-Year High Amid November Surge

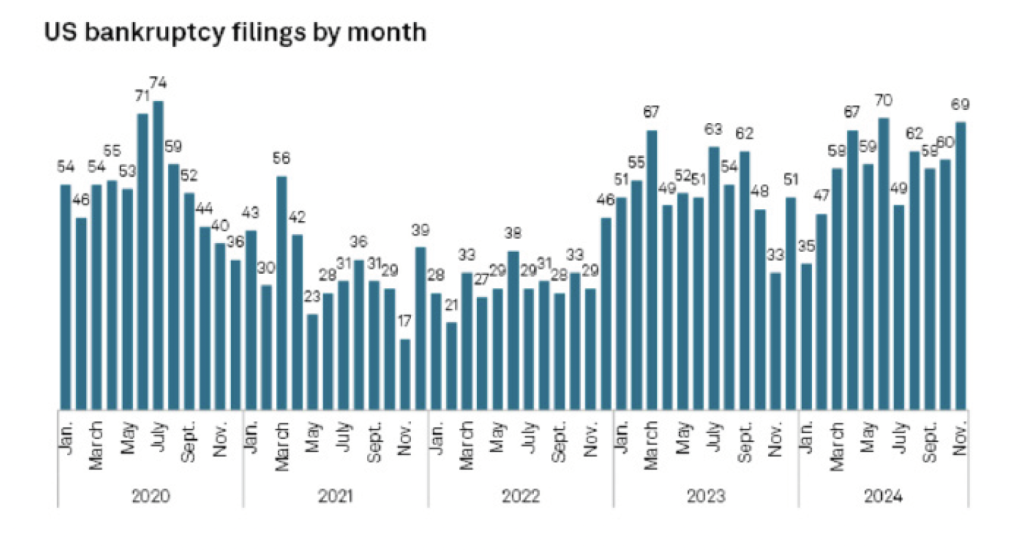

November saw a sharp increase in U.S. corporate bankruptcy filings, potentially driving the 2024 total to a 14-year high. According to S&P Global Market Intelligence, 69 public and select private companies filed for bankruptcy last month, making it the second-highest monthly total since early 2021.

Source: S&P Global Market Intelligence, Marketplace, Visual Capitalist

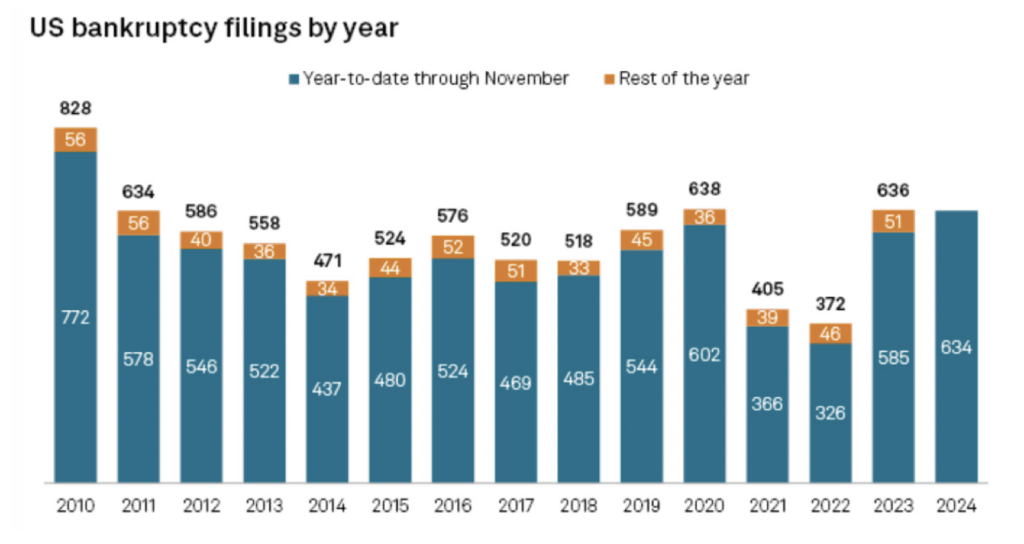

Over the past five years, bankruptcy filings typically slowed in November. This year’s spike contrasts with that trend, raising the year-to-date total to 634, nearly matching the full-year totals of 636 in 2023 and 638 in 2020. Should 2024 surpass those years, total bankruptcy filings during the year would amount to the largest single-year total since the aftermath of the Great Recession in 2010.

Moreover, bankruptcy filings have accelerated in 2024 as businesses face ongoing pressure from high interest rates, inflation and changing consumer spending patterns. While the US Federal Reserve has begun lowering its benchmark interest rate from a 20-year high, the pace of further cuts may slow in 2025 amid challenges posed by persistent inflation and potential tariffs introduced after the recent presidential election. However, the election outcome in November did provide an initial boost to stock markets and investor risk appetite.

Notable filings

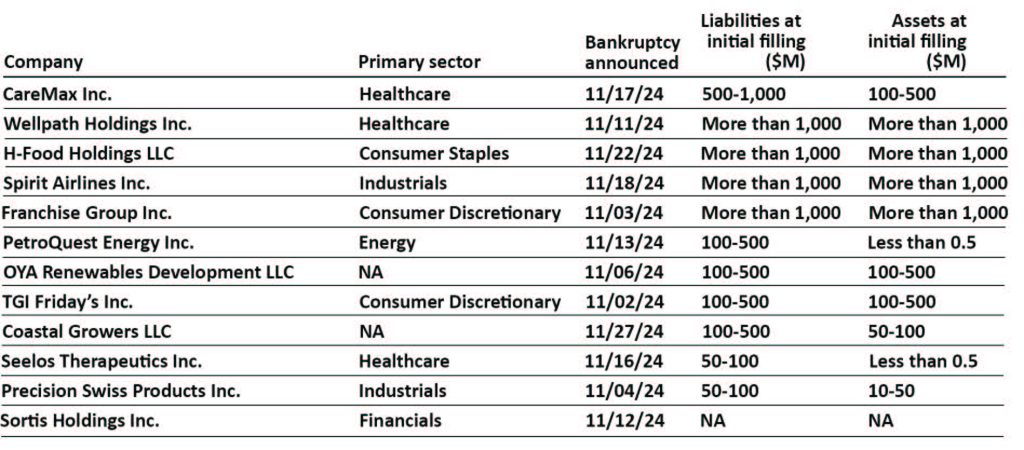

The four bankruptcies in November — each with liabilities exceeding $1 billion at the time of filing — were Chapter 11 reorganizations by H-Food Holdings LLC, Spirit Airlines Inc., Wellpath Holdings Inc. and Franchise Group Inc.

Franchise Group said Nov. 3 that it entered into a restructuring support agreement with the majority of its first-lien debt holders on a plan to strengthen the capital structure for its portfolio of brands, which includes furniture and specialty retail stores.

Similarly, healthcare provider Wellpath reached an agreement with most of its first- and second-lien lenders to sell one business segment and reorganize another, according to a company statement.

Data compiled Dec, 2024

NA= not available

Includes S&P Global Market Intelligence-covered US Companies that announced bankruptcy between Jan. 1, 2024, and Nov. 30, 2024, with liabilities of $1 billion or greater.

Source: S&P Global.

During its reorganization, budget airline operator Spirit Airlines received a $350 million equity investment

commitment from its existing bondholders and will complete a deleveraging transaction to equitize $795 million of funded debt, the company said Nov. 18.

H-Food Holdings, together with its packaged food manufacturing affiliate Hearthside Food Solutions, plans to reduce its debt load by more than $1.9 billion and secure $200 million of new equity capital through reorganization, according to a Nov. 22 statement.

Sector breakdown

Companies classified within the consumer discretionary and consumer staples sectors collectively accounted for 17 of November’s bankruptcy filings, as businesses with the most exposure to tighter consumer budgets continue to face the most economic pressure. Companies within the industrial sector filed 10 bankruptcies during the month.

Healthcare companies have filed 62 bankruptcies through the first 11 months of the year, the third-highest pace among the 11 sectors tracked by Market Intelligence. However, the sector added only three bankruptcies in

November. Year to date, about 276, or 44%, of all bankruptcies were filed by companies in the consumer discretionary, consumer staples, industrial or healthcare sectors.

CLAIM FILING KEY CONSIDERATIONS

Upfront due diligence: To help best assure a buyer is properly covered, make sure that the bill to name and address on your invoices matches the approved buyer limit provided by underwriting. Note that some policies provide group limits (only offered by a few select credit insurance carriers), so you may see coverage under a parent company name, however please review and confirm. The policy places the burden on the policyholder to make sure the correct buyer is listed.

Maximum Terms of Sale: Make sure terms of sale are not longer than what the policy accommodates.

Claim Filing Deadlines: Most policies specify a maximum time frame in which you can submit claims. Depending on the carrier, insolvency claims need to be filed within 30 days and slow payments within 180-365 days from ship date. Ask your agent or check your policy for your claim filing deadlines. We understand that often customers make promises to pay and you want to be helpful and supportive. If you are approaching a claim filing deadline and feel that with more time you can resolve matters, please contact us to ask for an extension of the filing deadline. We caution you against just waiting for promised payments when you are close to any claim submission date. If you miss the filing deadline and don’t request an extension or submit a claim, you will lose the past due coverage and possibly the ability to file an insolvency claim in the future.

Repayment Plan Approvals: Carriers do have the ability to approve payment plans that extend beyond the boiler plate terms when needed and effectively communicated. Be sure to have us secure underwriting approval of any repayment plan or compromise offer before you accept it or you will void your coverage.

Cease Shipment/Auto Cancel Provisions: Some policies require you to cease shipping if a covered account exceeds a certain past due threshold. Other policies may have provisions which automatically cancel forward coverage once these thresholds are reached. Be sure to read your policy and note any such conditions.

Past Due Reporting Requirements: Some policies have past due reporting requirements (i.e. greater than 60 days past due). Be sure to read your policy and note any such conditions.

Proof of Claim: On some policies, a proof of claim must be filed by the policyholder in the event of an insolvency. Be sure to check your policy to determine if your carrier requires this or if they handle for you as part of the claim process.

Actions to Minimize Loss: In slow payment scenarios, the policyholder always wants to demonstrate that they have taken prudent steps to minimize exposure and mitigate a loss. This may include ceasing shipments, utilizing third party collections resources, and documenting your internal collection efforts.

Required Documentation: Current Aging; Purchase Orders; Invoices; Proof of Delivery; If applicable, documentation you received on the debtor’s bankruptcy or receivership; Correspondence – any related communication with this debtor, collection efforts, written confirmation of the debt from the debtor.

We encourage you to contact us or your agent directly if you experience any payment issues with a covered account. We will be happy to discuss best next steps to help protect your coverage.

Tip 1: Send invoices out on a regular basis.

This might seem simple and straightforward, but it’s essential. Establishing predictability is key. Buyers can’t pay if they haven’t been billed, so it’s important to develop a consistent rhythm they can rely on. This approach benefits both your buyers and your internal team.

Tip 2: Use accounts receivable payment terms as a rule, not a guideline.

You might have entertained the idea that rules are made to be broken, but that’s not the case when it comes to payment terms. To ensure timely payments, you must set clear expectations from the start: payment terms are non-negotiable. If payment is due in 30 days, it means 30 days. Be friendly yet firm—your company is a priority for you, and your buyers should feel the same. Establish your expectations early and consistently reinforce them throughout the relationship.

Tip 3: Educate your accounts receivable team.

We often hear the phrase, “An educated customer is your best customer.” But have you considered: what about your team? Are you investing time in educating them? Train your staff on why maintaining a consistent rhythm is critical, and ensure they know how to handle situations when someone doesn’t follow the rules. Habits become second nature. Teaching your team to navigate these interactions empowers them to uphold your standards.

Here’s something to think about: if your competitor has a well-established rhythm and process for accounts receivable collections and you don’t, which company is more likely to get paid first? Set clear guidelines for your team’s actions and help them understand what’s needed to protect one of your company’s most valuable assets: your accounts receivables.

Tip 4: Establish standards for your core accounts receivables best practices

It’s no secret that problems will arise sooner or later, so when non-payment occurs, it shouldn’t catch anyone off guard—not you or your team. Your training should prepare your team to handle these situations by covering: • How to create accurate supporting documentation for claims. • How to draft contracts proactively, before late payments become an issue. • Steps to take when legal action appears to be the only option. • Regularly reviewing credit processes to identify and implement improvements. • Enforcing updated credit processes to ensure they become standard practice.

By establishing these practices, you can effectively safeguard your business against non-payment, both through preparation and in execution.

Source: Allianz Trade

Every industry faces unique credit risks shaped by its specific market dynamics, customer behaviors, and operational challenges. From long payment cycles and seasonal volatility to rapid innovation and supply chain complexities, these risks can significantly impact cash flow and financial stability if not managed effectively. Recognizing and addressing these challenges is critical to safeguarding your business against potential disruptions. Here’s a deeper look at the specific risks in key sectors.

1. Construction Industry: Managing Long Payment Cycles and Funding Gaps

In the construction industry, payment cycles can stretch for months due to project-based contracts and complex payment structures. Delays in project funding or disputes can lead to cash flow issues and increased risk of non-payment. Trade credit insurance provides a safety net, ensuring that even if a contractor or subcontractor defaults, your cash flow remains protected.

2. Retail Industry: Mitigating Seasonal Volatility and Market Pressures

Retailers depend heavily on seasonal sales peaks, such as the holiday season. If demand falls short of projections or major buyers fail to pay after placing large orders, the ripple effects can be devastating. Trade credit insurance safeguards your accounts receivable, ensuring your business remains stable even in the face of unexpected seasonal downturns.

3. Manufacturing Industry: Navigating Supply Chain and Payment Risks

Manufacturers often extend credit to multiple buyers while relying on complex supply chains that are vulnerable to disruptions. When a buyer’s financial instability leads to non-payment, it can affect your ability to purchase raw materials or meet production deadlines. Trade credit insurance minimizes the impact by compensating for unpaid invoices, keeping your operations running smoothly.

4. Technology Sector: Balancing Innovation and Credit Risk

The technology sector is marked by rapid innovation, short product lifecycles, and a high number of startups with limited credit histories. Extending credit to such buyers can be risky, especially when their financial footing is uncertain. With trade credit insurance, you can confidently support these buyers, knowing your receivables are protected.

Tailored Solutions for Your Industry

Credit risks doesn’t look the same across industries, which is why a one-size-fits-all approach doesn’t work. Trade credit insurance can be customized to address your sector’s specific challenges, providing the protection you need to grow confidently while minimizing financial risks.