Balancing Economic Risks and Political Change

Economic Update

For November, the U.S manufacturing rate was 48.4% on the ISM Index, 1.9% higher than the October reading. Any reading under 50.0% is contractionary. Activity contracted at a slower rate than in the previous month but is still attributed to continued weak demand and declining output. The unemployment rate was little changed at 4.2% in November, adding 227,000 jobs. The report presents a picture that the labor market has slowed but is still doing well.

State of Corporate Credit

Weakest link companies, which are companies rated ‘B-‘ by S&P, showed a negative bias for the year. While this may seem positive on the surface, the result was driven by a higher number of defaults rather than upgrades to their credit ratings. On a positive note, upgrades have outnumbered downgrades for investment grade rated entities.These trends highlight how high-risk companies are struggling with lower consumer spending elevated interest rates, and other economic headwinds, while low-risk companies continue to prosper. Metals, Mining and Steel showed a potential of 16 downgrades by S&P compared to a potential of 8 upgrades.

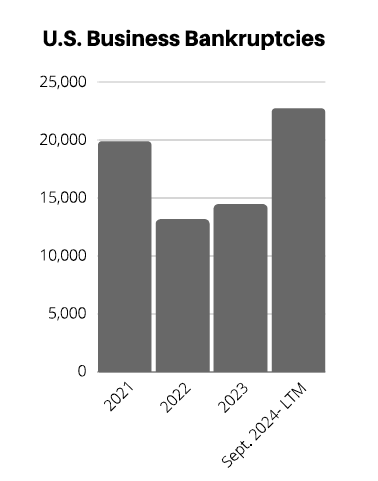

Insolvencies

U.S. Corporate bankruptcy filings jumped in November 2024, which will likely push the yearly total to a new 14-year high. November marked the second most bankruptcies filed in one month since early 2021. Additionally, it is important to note the recent increase in default rates for consumers, especially; for credit cards and auto loans, which highlights the ongoing financial strain among households. Given the U.S. economy’s deep reliance on consumer spending this trend could further ripple across and impact a wide range of economic sectors. In Canada, business insolvencies for the 12-month period ending October 31, 2024, increased by 10.9% compared with the same period last year.

Current & Evolving Credit Risks

Supply Chain Risks

Proposed tariffs could disrupt supply chains, leading to increased business expenses, higher consumer prices, and extended cash flow cycles. Supply chain disruptions can negatively impact credit quality by causing revenue loss, increased costs for alternative sources and logistics, reduced cash flow due to longer payment cycles, higher debt to finance working capital, and decreased financial and operational visibility. However, we note that some companies would be poised to benefit from certain tariffs, such as domestic steel producers.

European Outlook

The economic outlook for Europe has worsened, with business confidence declining recently. Additionally, headline inflation increased for the second consecutive month, reaching 2.3% in November, creating a challenging stagflationary environment (high inflation, low economic growth, and high unemployment). Furthermore, continued geopolitical instability remains a top credit risk for the region.

Metals Sector Updates

In the ISM survey, businesses in the fabricated metals products sector indicated that business is slowing due to customers reducing inventory and uncertainty about future demand. Initial forecasts for 2025 were lower but may improve now that the U.S. election is over.