Insolvency Surge Continues

Economic Update

For September, the U.S. manufacturing rate was 47.2% on the ISM Index, the same as August. Any reading under 50.0% is contractionary. The continued contraction is attributed to subdued demand and declining output. The unemployment rate fell to 4.1% in September, adding 254,000 jobs. The report pushes aside concerns of a sudden deterioration in labor market conditions.

State of Corporate Credit

Driven by strong issuance volumes, rated corporate debt in the U.S. has increased by 3.7% over the last twelve months to July 2024, compared to 1.4% growth over the same previous year period. Investment grade-rated debt increased the most, by 4.4% as well-capitalized companies continue to utilize debt for growth. Speculative grade debt increased by 1.7%, as high-risk companies grapple with lower demand and tighter financing conditions. For the metals, mining, and steel sectors, total outstanding speculative-grade debt is 31.8% higher than investment grade, at $40.3 billion compared to $30.7 billion, respectively.

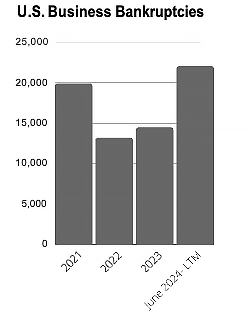

Insolvencies

Commercial Chapter 11 filings increased by 33% in September 2024 when compared to the same period last year, nearing pandemic highs. The rise in bankruptcies is expected to continue, as companies face declining demand in certain industries, like automotive. Recent bankruptcies impacting the industrial sector include Accuride Corporation and Wrena, LLC. In Canada, business insolvencies for the 12 months ending August 31, 2024, increased by 51.6% year over year. Accommodation and food services, Construction and Transportation, and Warehousing registered the biggest increases in the number of insolvencies. Mining quarrying and oil and gas extraction all decreased.

Current & Evolving Credit Risks

Steel Pricing

Prices for hot-rolled coil (HRC) steel have decreased nearly 40% since the beginning of the year, currently standing at $696 per ton. This decline in pricing is primarily attributed to stagnant manufacturing activity, reduced construction spending, and decreased steel consumption in China.

Default Risk

Falling interest rates may not provide the anticipated relief for issuers facing upcoming maturities who have yet to refinance. Selective defaults-situations where a company is unable to sustain its capital structure at current rates and must undergo restructuring have increased at more than double the rate observed prior to the pandemic.

Labor Strike

Boeing’s strike, now in its 5th week, is crippling the company and supply chain. Boeing withdrew its latest offer and laid off 10% of their workforce. While the strike is unlikely to jeopardize the stability of larger, well-capitalized suppliers, smaller companies face significant risks. While the Dockworker’s strike was suspended recently and a tentative agreement is in the works, the union still has disagreements regarding the use of automation at ports. Strikes are very disruptive and if prolonged can create non-payment issues for companies impacted.